2-5: How hedge funds use the CAPM

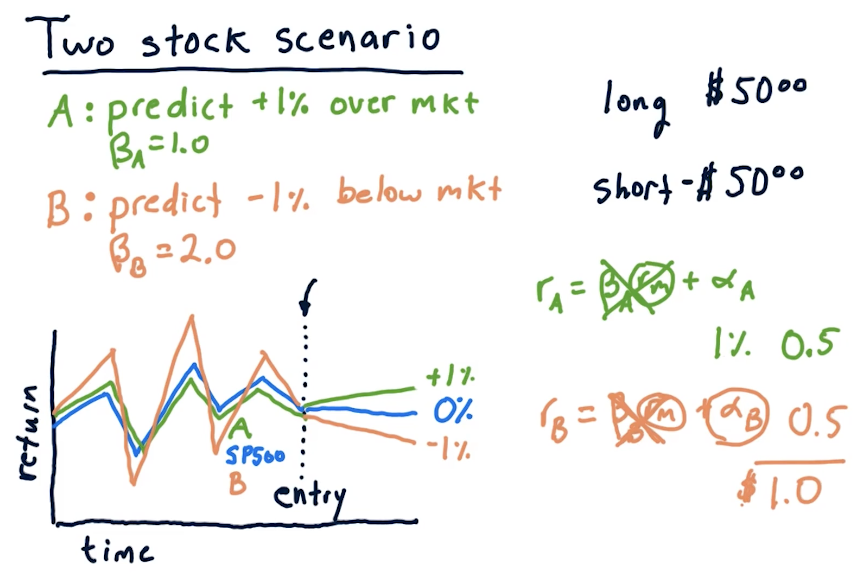

Two stock scenario

In this scenario, we've used some machine learning model to predict that a particular stock, A, will be +1% over the market and stock B will be -1% below the market. Given this, we take a long and short position to make a profit. A high-level overview from the lectures on how to calculate these returns using beta under these circumstances is provided below:

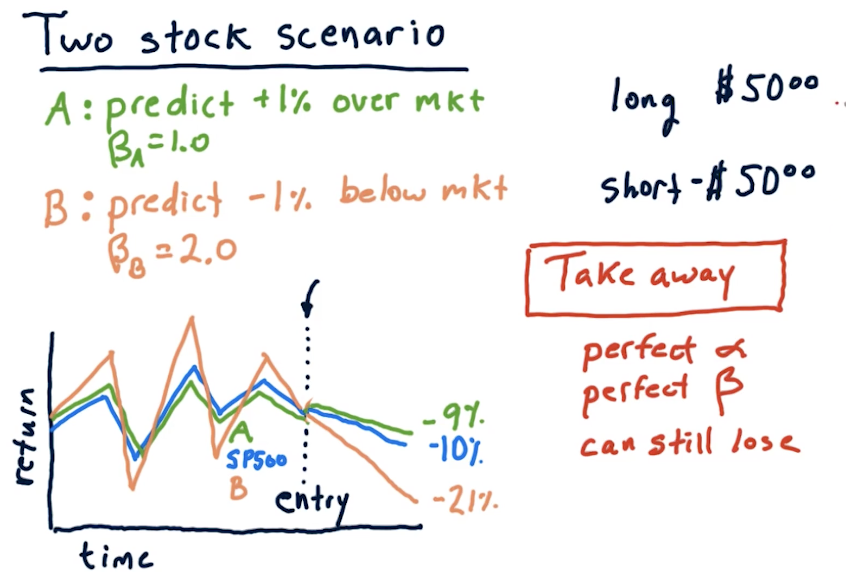

Two stock takeaways

The below snippet from the lecture reinforces that, if we're not careful with how we allocate our money, we could end up losing money taking short positions in an upward trending market, and losing money taking long positions in a downward trending market. Basically, you need to hold the right stocks with the right beta for the right market.

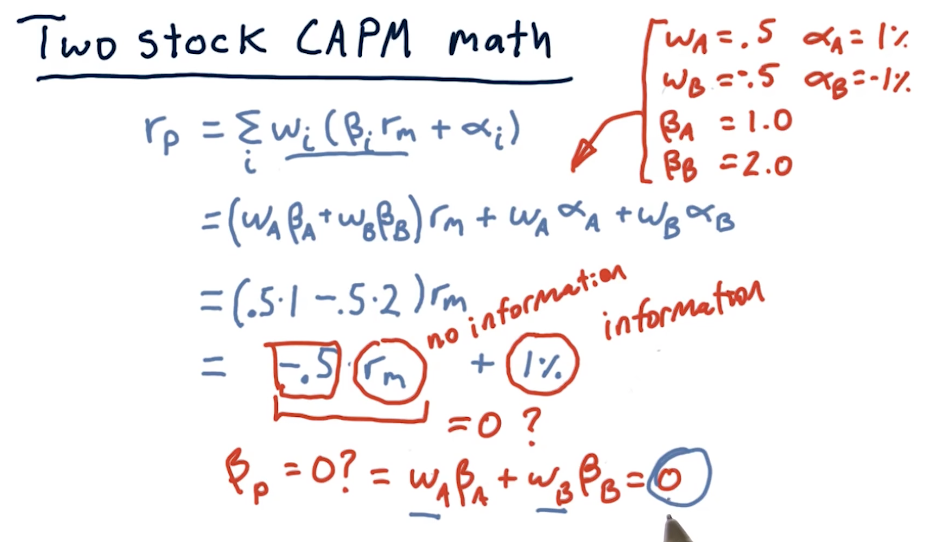

Two stock CAPM math

The lecture takes the examples provided earlier and uses CAPM to simplify the math into a regression equation. The point of this lecture is to state that we can remove market influence on our portfolio if we aim to minimize beta to 0.

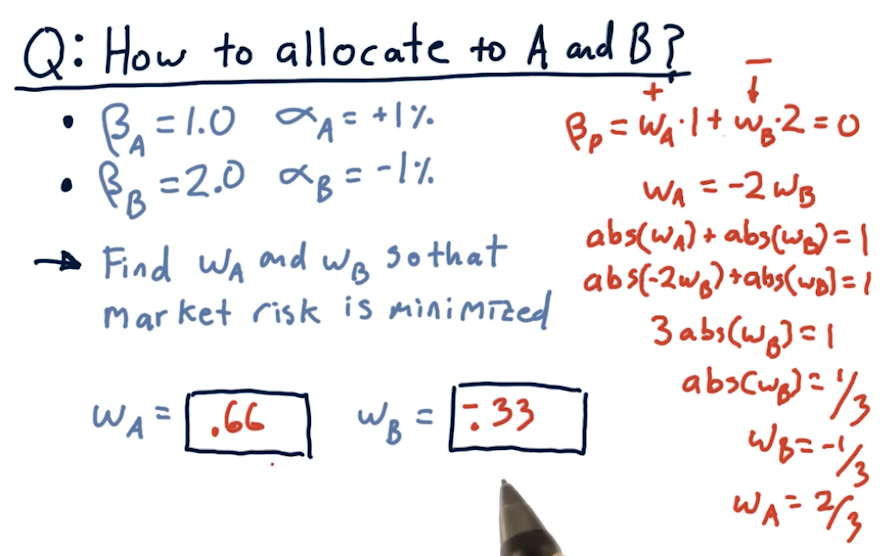

Allocations to remove risk

The lecture covers how to calculate allocations, W[i], to remove risk from a

portfolio.

Wrapping up

The lecture covers how to calculate returns when the market has a 10% increase, given the allocations we calculated previously to remove market influence on the portfolio.