1-4: Statistical analysis of time series

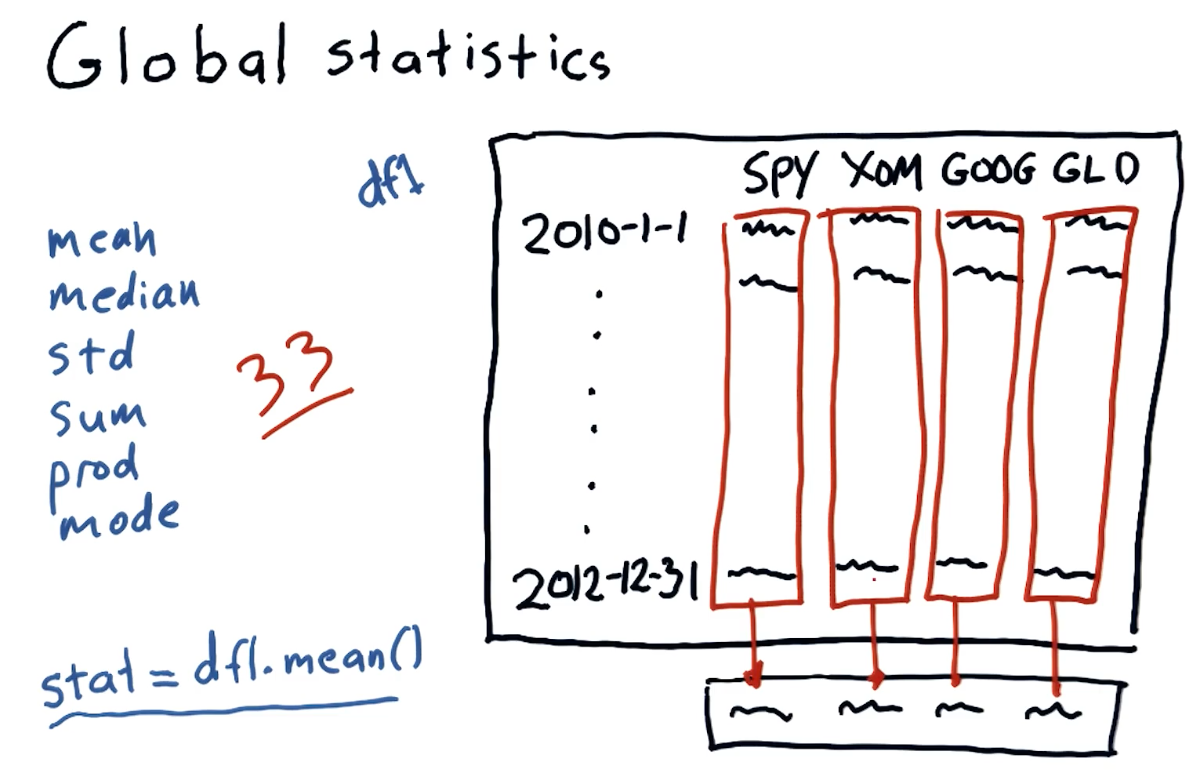

Global statistics

We can easily compute global statistics like mean, median,

standard deviation, and more using pandas dataframes. A high-level

interpretation provided in the course lecture is provided below:

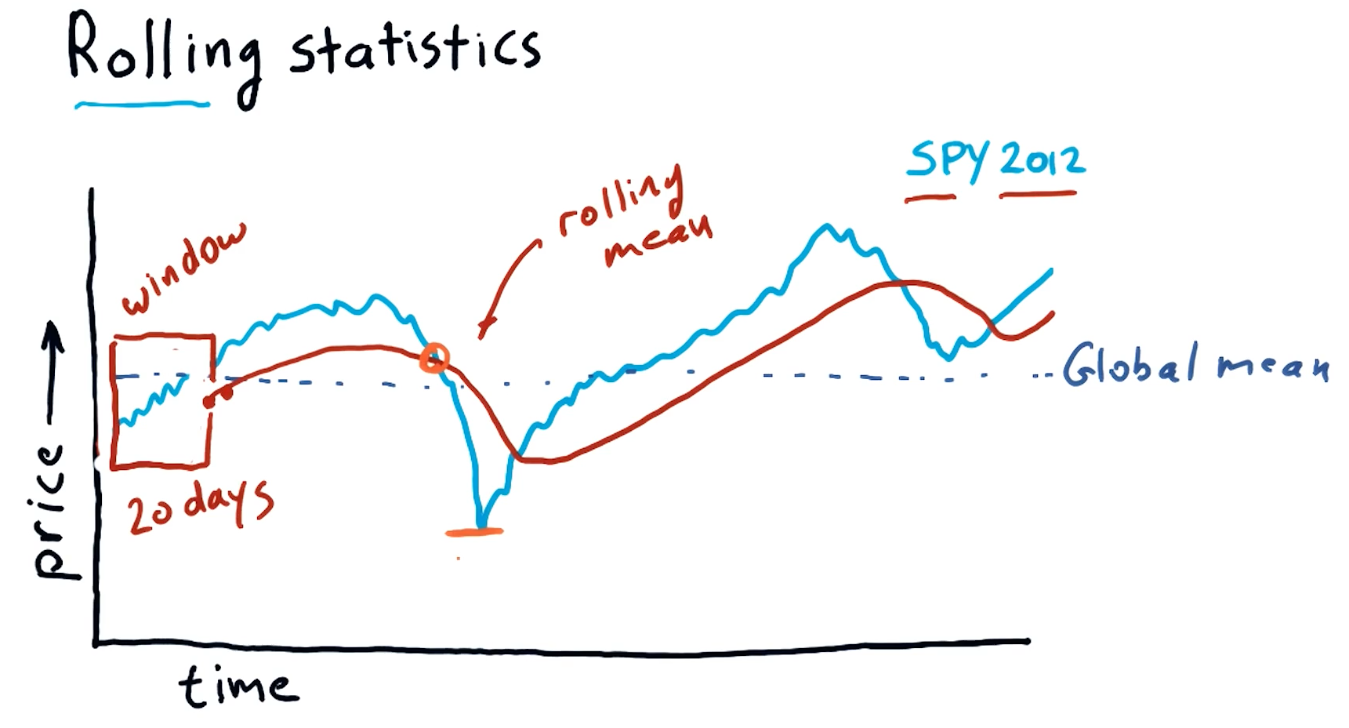

Rolling statistics

Rolling statistics are statistics observed during a time-slice of the global data. These rolling statistics allow us to derive trends from the global data. A high-level interpretation provided in the course lecture is provided below:

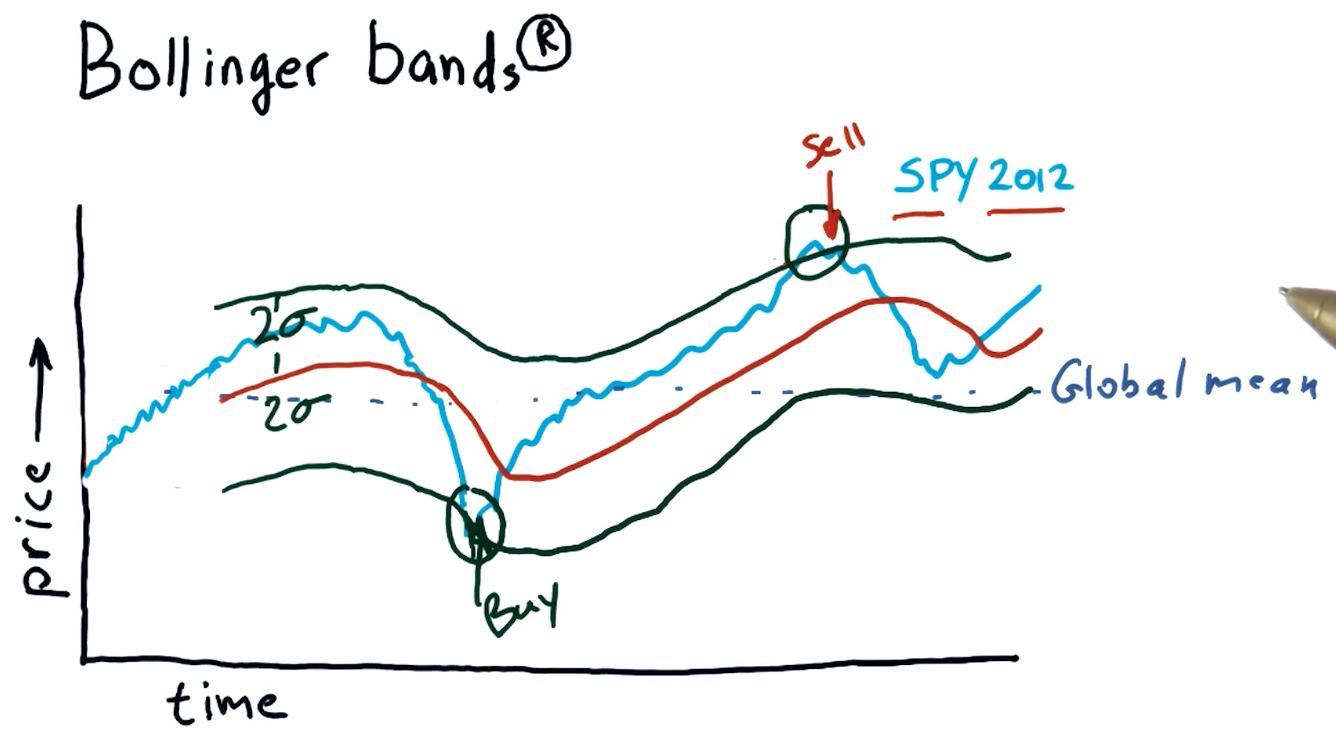

Bollinger bands

Bollinger bands are a trading concept where we maintain a rolling mean and define two bands that are separated two standard deviations from the rolling mean in both directions. Once a stock's value crosses below the lower threshold and then crosses above it, we can consider this a buy signal. Similarly, we can detect a sell signal when a stock crosses above the higher threshold and begins to dip below it. A high-level interpretation provided in the course lecture is provided below:

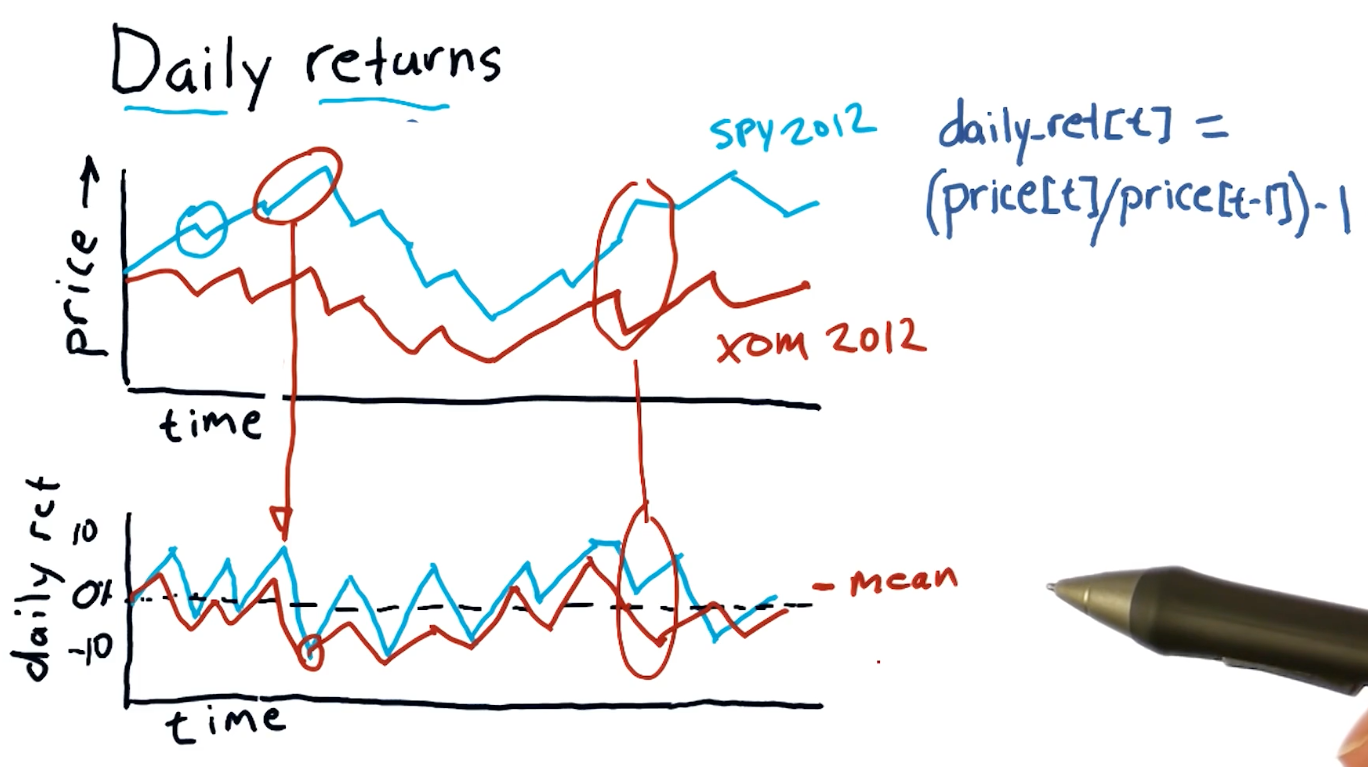

Daily returns

Daily returns can be easily calculated using the following equation:

daily_ret(t) = (price[t] / price[t-1]) - 1

Where t == date.

A high-level representation of daily returns from the course lecture is provided below:

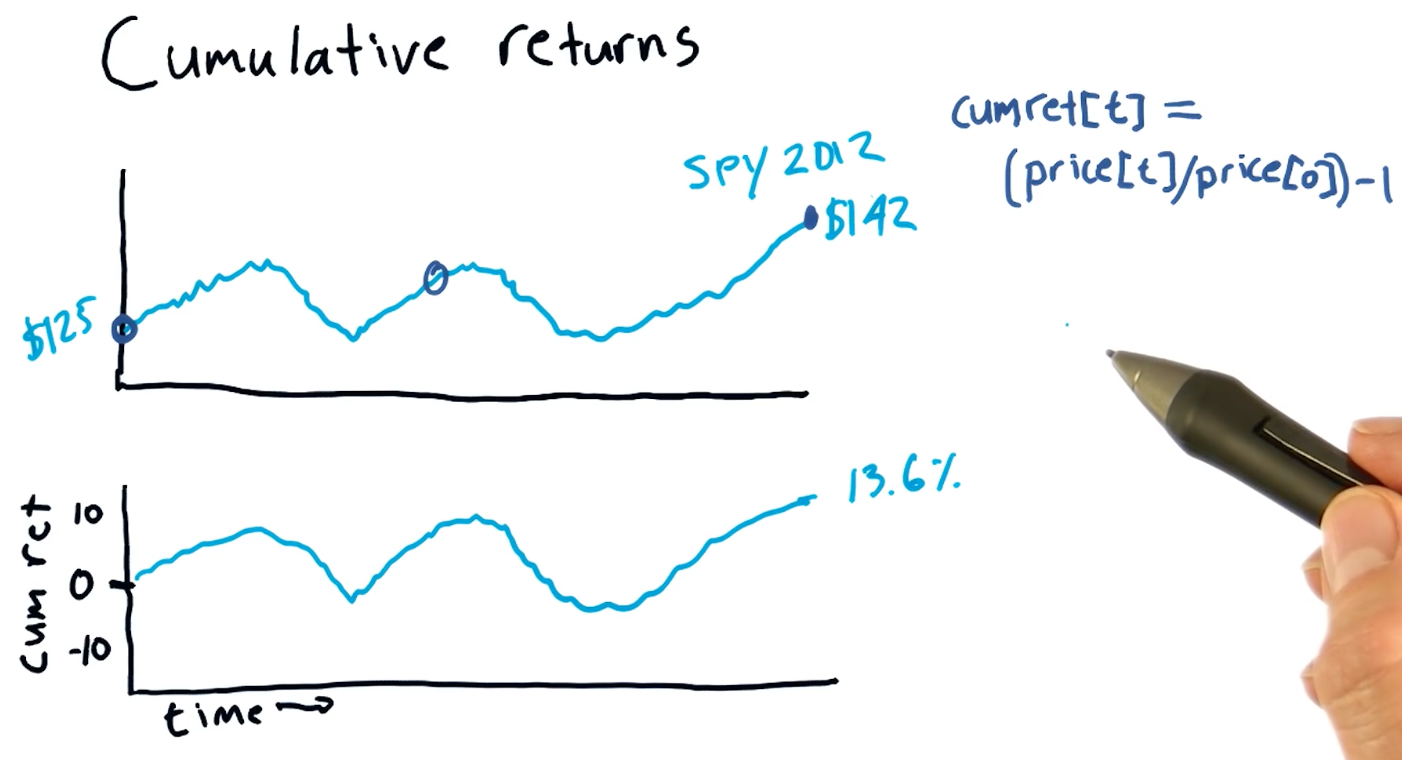

Cumulative returns

Cumulative returns can be easily calculated using the following equation:

cumulative_ret(t) = (price[t] / price[0]) - 1

A high-level representation of cumulative returns from the course lecture is provided below:

Quizzes

Which statistic is best to use to determine buy / sell signals?

- rolling sum

- global mean

- global max

- rolling standard deviation