1-9: How to optimize a portfolio

What is portfolio optimization?

Given a set of assets and a time period, find an allocation of funds to assets that maximizes performance.

What is performance?

We can choose from a number of statistics such as:

- Cumulative returns

- Volatility or risk

- Risk adjusted returns (Sharpe ratio)

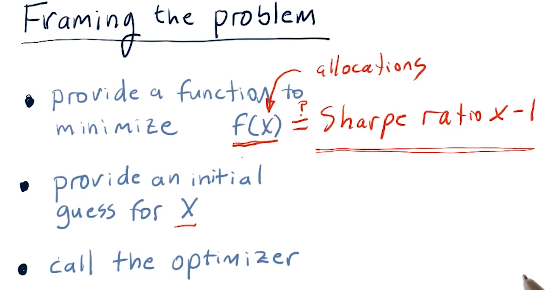

Framing the problem

So how do we go about optimizing a portfolio? We use an optimizer to find the inverse Sharpe ratio for a given set of allocations in a portfolio. A high-level representation provided by the lecture is provided below:

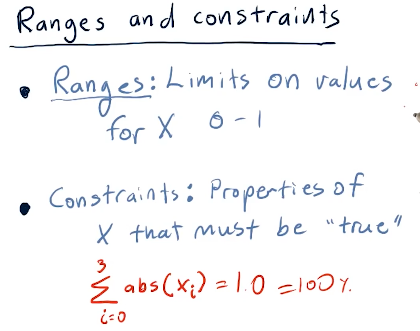

Ranges and constraints

Ranges and constraints on the values of X provided to the optimizer for the

function to be minimized can help speed-up the rate at which the optimize can

solve the minimization of the function. Ranges in this case should be

limited from 0 to 1 as these represent percentages. Constraints in this

example specify that the sum(x) should equal 100 - meaning our allocations

reach 100% for an effectively optimized portfolio. Below is the slide from the

lecture discussing this topic: